I recently caught wind of an interesting Cointelegraph article explaining how investors could earn 41% APY on their Bitcoin without converting it to renBTC or WBTC.

In the article, the writer laid out a detailed case for generating yield on Bitcoin (BTC) holdings by investing in options markets instead of decentralized finance (DeFi) apps.

While we are proponents of this exact strategy some of the explanations laid out in the article are more confusing than useful so I want to add a little clarity to the best way to execute this strategy.

How Do Covered Calls Work?

In the article, the author describes a covered call strategy as consisting of “simultaneously holding BTC and selling the equivalent size in call options.”

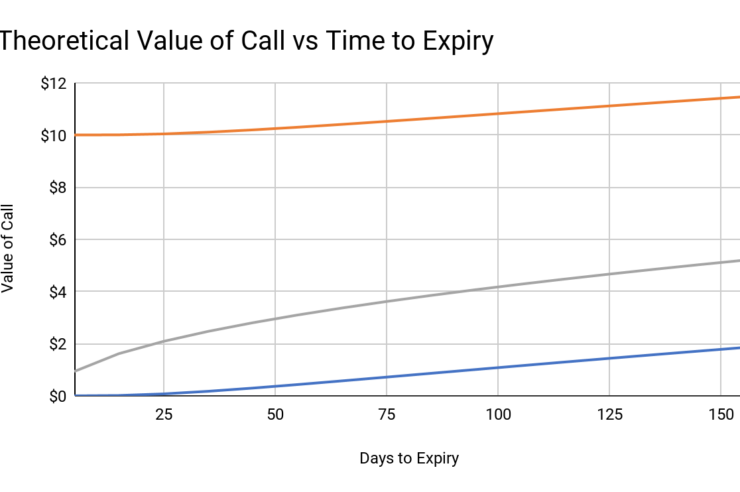

When selling the calls against your long BTC you receive the call premium, which is the price the buyer pays for the option to buy BTC at the strike price specified in the call option contract. The returns on a covered call strategy, then, depend on the premium you can generate.

Options premiums are difficult things to understand and it’s worth mentioning that Myron Scholes and Robert Merton won a Nobel Prize in 1997 for figuring out a reliable way to price them. But generally, the premium increases when the contract length is longer, when the difference between the price today and the strike price is smaller, and when BTC’s volatility is higher.

Relationship of call premium to contract length and the difference between today’s price and the strike. Source: Ryan Anderson

As shown above, the most lucrative covered call strategies will be the ones that have contract lengths greater than a year, strike prices equal to (or less than) today’s price, and are created when BTC volatility is highest.

At the time of writing, a call option which expires in June of 2021 and is struck at $10,000 BTC offers an annualized premium of 34.66%. This is even after considering BTC volatility is rather low these days compared to historicals.

BTC volatility since spring of 2019. Source: Skew.com

However, it’s important to recognize the risks associated with different covered call strategies.

An easy way to visualize the exposure you get when trading options is to look at profit and loss on your position versus where the BTC price ends up on the day the contract expires.

P&L charts for long stock and long call positions. Source: Investopedia

By way of comparison to just being long on a stock, being long on a call is different because your downside is capped. You only ever lose the premium you paid for the call, but when the price of the asset is above your strike, you profit.

A covered call is a position made by going long an asset and short a call option on that asset, so the combined profit and loss looks something like the below.

P&L chart for a covered call. Source: Investopedia

The exposure looks like a long asset exposure, with uncapped downside, until the strike price of the option.

When the asset price is higher than the strike price at expiration, the call gets exercised and you sell your asset to the buyer.

Because the investor owned the asset the entire time, this is not a loss in profit and loss terms, and so the upside exposure is merely capped.

The Trouble with the previous proposal

Here’s where we ran into some problems with the article’s framing of how to trade options. The author suggests that in comparison with DeFi-based yields:

“Trading BTC options at Chicago Mercantile Exchange (CME), Deribit, or OKEx, an investor can comfortably achieve 40% or higher yields.”

But when above we looked at essentially the best-case covered call we found that its annualized premium reached 34.66%. So where’s the difference?

The author based the 40% figure on one call contract expiring at the end of November 2020 with a strike at $9,500. This strike price is lower than today’s price for BTC, which is about $10,750 per BTC. According to the author:

“As previously mentioned, the covered call might present losses if the BTC price at expiry is lower than the strategy threshold level….Any level below $8,960 will result in a loss, but that is 16.6% below the current $10,750 Bitcoin price.”

This, unfortunately, is a fundamentally mistaken way of thinking about covered calls. If an investor sells a call option with a strike price lower than today’s price (or the price the investor expects the asset to hold at day of expiry), they must be ready to sell your asset at that lower strike price.

Put another way, if one holds 1 BTC today, when the price is $10,750, and then sells a call against it at a $9,000 expiry today, the lucky person on the other side gets to make a free $1,750 when they buy the BTC from the investor at $9,000.

The author offers another set of strikes to consider, this time at $8,000 and $9,000, but the same error is committed when describing the profit and loss.

In the article the author says:

“A 25% APY return can be achieved by selling 0.5 BTC $8K and 0.5 BTC $9K November call options. By reducing expected returns, one will only face negative outcomes below $8,370 at the November 27 expiry, 22% below the current spot price.”

This is mistaken again. Agreeing to sell at $8,000 when BTC is trading at $10,750, unless you have a real belief that the price at expiry will be below $8,000/BTC, is a negative outcome!

From our experience, when an investor enters a covered call position, we believe they maximize their expected return when leaving a little room for upside performance in BTC.

That’s why we favor selling about 20% higher than today’s price. What’s equally important, though, is the length of the option contract.

Know your ‘options’ when trading options!

Trading options on a less than monthly basis introduces some extra risk due to liquidity. In general, the most liquid contracts are the monthly expiries, a pattern that holds equally as well in crypto markets as in traditional markets, like equities, commodities, and foreign exchange.

The author had set his call to expire at the end of November, which is a two-month contract. That’s ok from a liquidity standpoint, but that length neither maximizes the premium generated like a very long-dated contract would not minimize risk from length of contract like a one-month contract would.

BTC Options OI by Expiry. Source: Skew.com

For that reason, we favor a strategy that involves trading one-month options. The major benefit of trading covered calls monthly is that investors reset their strike price every month.

Selling calls 20% higher than today’s price is a dicier proposal if one has to wait two months or longer to reset, but when with resetting every month, the gains are also capped at 20% per month.

Even BTC, the most volatile asset class by far, is rather infrequently growing by more than 20% per month. By contrast, 20% price moves over two months or longer are almost to be expected.

Options trading is difficult and demands sophistication and forethought from the investors who seek to profit from it. While other strategies may offer higher headline returns at the expense of less-understood risks.

As is always the case, investors should do their own research before making any investment decisions.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Ryan Anderson is the head of trading at Wave Financial Group. Before joining Wave Financial Group in 2019, Ryan was a research associate at Bridgewater Securities and trader at Goldman Sachs. Ryan received his BA from the University of Pennsylvania. Wave provides investable funds via their diverse investment strategies applied to digital assets and tokenized real assets. The group also offers managed accounts for HNWIs and family offices seeking tailored digital asset exposure, bespoke treasury management services, and early-stage venture capital and strategic consultation to the digital asset ecosystem.

{kind=link}

{kind=link}

Comments (No)